4 key points to keep in mind following the US central bank’s meeting

1.Done!

Following 7 years of unchanged rates, the Federal Reserve has, as expected, raised its interest rate range from 0-0.25% to 0.25-0.50%. This decision was widely anticipated because several statements from members of the Federal Market Open Committee (FOMC) had prepared the markets for an increase. The FOMC members remain relatively confident in their expectations for the US economy and the wider context now seems of less concern, prompting them to take action.

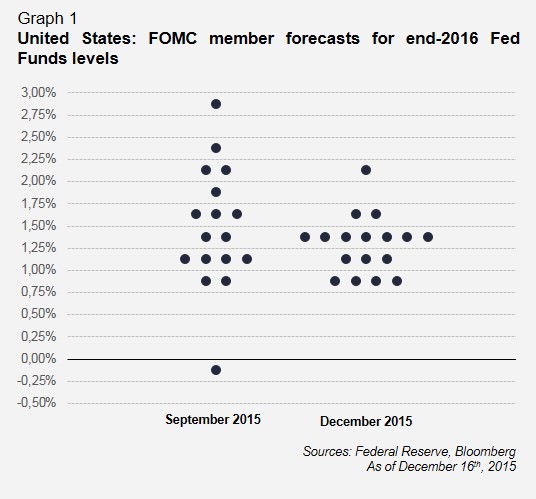

We note that in preparation for this “challenge” Fed members felt the need to realign their opinions: the decision was unanimous and forecasts were much closer than at the last committee meeting. Yet it is unlikely that recent economic developments will have altered the view of a ‘hawk’ like Jeffrey Lacker to the point of actually getting him to lower his rates estimate by 75 basis points for the end of 2016. This shift probably therefore reflects a concerted effort by FOMC members to present a more united front at this crucial time.

2.The right balance

One of the challenges for Janet Yellen was to get the market to accept the increase without giving too much in exchange. She may well have been successful:

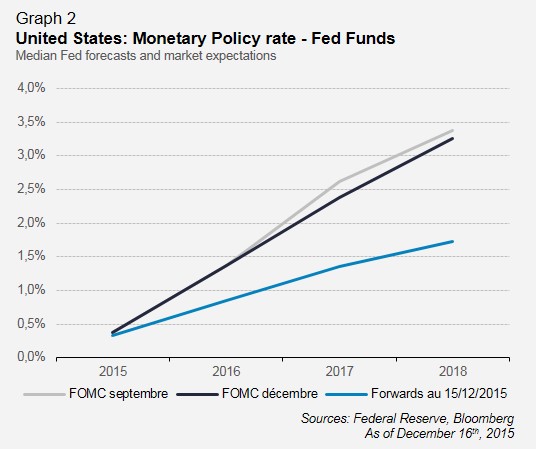

- the median points have hardly budged and still imply a pace of four increases in 2016. Only 2017 and 2018 were revised marginally downwards.

- the markets reacted well with relatively stable rates and currencies and a reasonable increase in the equity market.

3.A first rate hike out of the way – but there’s more to come

During the press conference, Janet Yellen sought to describe the shape of things to come. She put particular emphasis on what she meant by gradual, insisting on the fact that the rate increases would not be mechanical in timing or magnitude. The rate hike will be gradual because the increase in the neutral funds rate will also be gradual (the neutral rate, which is consistent with stable inflation in an economy operating near potential, is currently very low because of several headwinds which should abate over time).

So the challenges ahead are starting to emerge: with very low long-term rates, the Fed is seeking to avoid the alarm that could provoke a bond market crash, hence the concept of gradualism. Even so, in light of the disappointment it faced with the mechanical rate hike cycle of 2004-2006, the Fed is seeking a degree of freedom similar to 1994, when the upward cycle was successful in that it ended with a soft landing for the US economy. However, 1994 was a dark year for the bond markets. Janet Yellen repeated several times that delaying monetary policy normalisation was running the risk of having to raise rates abruptly, increasing the risk of recession. As always, the Fed is aiming for a soft landing.

4.Towards a change in the Fed’s reasoning?

During the press conference, Janet Yellen explained that although the neutral rate was set to rise over time, the pace of the normalisation was still unknown and could be slower or faster than expected. This is why the Fed will closely monitor economic indicators such as employment, wages, and inflation.

Up to that point, the Fed’s statement is nothing out of the ordinary. It traditionally focuses on leading indicators in recognition that it takes time for monetary policy actions to affect future economic outcomes. However, considering its “model” of the US economy to be currently somewhat uncertain, it will be lending greater importance to incoming data on inflation

To sum up

Janet Yellen passed the test. The Fed is maintaining its desire to normalise monetary policy by 2018 whilst retaining a certain degree of flexibility in how to achieve that goal. By clearly stating that she will be taking published data into account, Janet Yellen should manage to coax bond markets into reacting according to published economic data. Indeed, as she herself reiterated, this first increase in rates was not that significant.

The real questions have yet to be answered: which path will the Fed Funds rate take in the years ahead? Will the Fed assert its freedom? How will the bond market react after twenty years of relative certainty?

This document is not pre-contractual or contractual in nature. It is provided for information purposes. The analyses and descriptions contained in this document shall not be interpreted as being advice or recommendations on the part of Lazard Frères Gestion SAS. This document does not constitute an offer or invitation to purchase or sell, nor an encouragement to invest. This document is the intellectual property of Lazard Frères Gestion SAS.